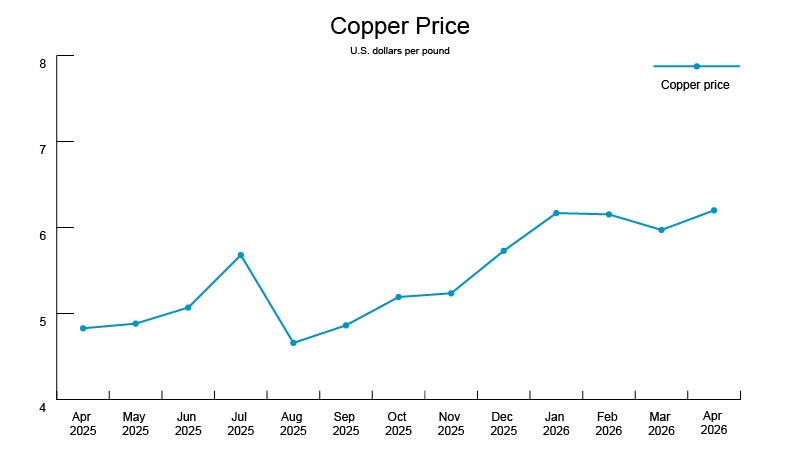

Copper’s push and pull by supply and demand forces

Copper prices remain volatile following January’s record highs and continue to fluctuate amid the conflict in the Middle East, with the closure of the Strait of Hormuz impacting both supply and demand dynamics.

Why it matters: The strait’s closure creates conflicting forces for copper — there are supply risks due to higher energy costs, but weaker demand if elevated energy prices slow global manufacturing. Inflation is nearing 4% and putting additional upward pressure on energy prices.

By the numbers: This morning, copper opened at $6.27. The year-to-date average price for copper is $5.80, up from $4.82 in 2025.

Supply side: For 2026, the average price forecast remains just above $12,100 per ton driven by concentrate shortages and limited new mine supply.

- Tightness in copper concentrates, reflected in historically low smelter treatment charges, is expected to limit refined copper production growth to just 0.4% this year.

- Global mine production rose only 0.9% in 2025 following major mine disruptions, according to the International Copper Study Group (ICSG). Expected mine growth for 2026 was revised down to 1.6% due to the lingering impact of those disruptions.

Yes, but inventory is at a historical high; total inventory across the three major exchanges rose to more than 63,500 metric tons in February. Glencore reported in April that its copper production in the first quarter exceeded its target, rising 19%, highlighting high inventory.

Demand side: The ICSG and Goldman Sachs revised their copper forecast for 2026, citing the conflict disruption and its potential impact on global economic activity.

The bottom line: These factors underscore the copper market’s delicate balance between supply risks and demand concerns.

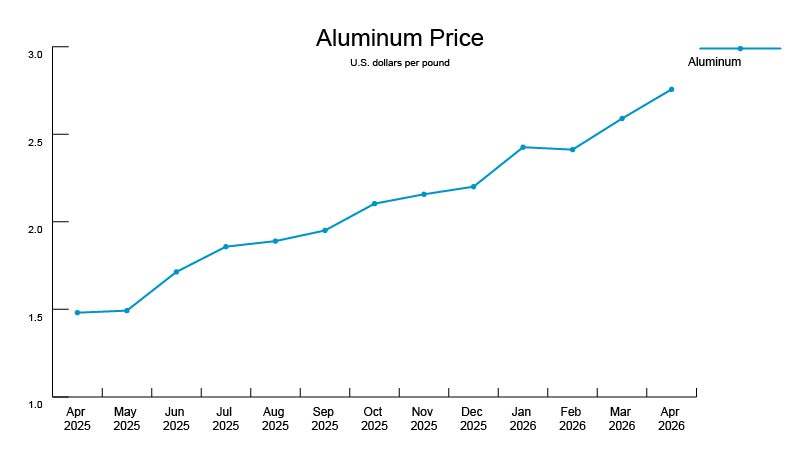

Aluminum faces major supply shock

The global aluminum market continues to experience a significant supply shock. Disruptions tied to the conflict in the Middle East are driving expectations of shortages this year, according to metals analysts at Mercuria.

Zoom in: The supply shock is impacting key industries, including automotive, which is also facing a 50% U.S. aluminum tariff, and the construction and packaging industries. The effects are especially pronounced in the United States and Europe, which rely heavily on aluminum from the Persian Gulf region.

By the numbers: The Middle East accounted for nearly 22% of U.S. imports of primary and alloyed aluminum in 2025 and more than 18% of European imports. And approximately 9% of global aluminum supply comes from the Middle East. Mercuria estimates a minimum deficit of 2 million tons this year, with benchmark prices on the London Metal Exchange reaching a four-year high of $3,672 per ton in mid-April.

Norsk Hydro reported quarterly core profits exceeded expectations as higher aluminum prices offset weaker alumina prices.

Between the lines: The disruption underscores the West’s continued reliance on the Gulf’s aluminum supply as rising premiums and reduced exports strain the market and aluminum-dependent industries.

Today, aluminum opened at $2.71.

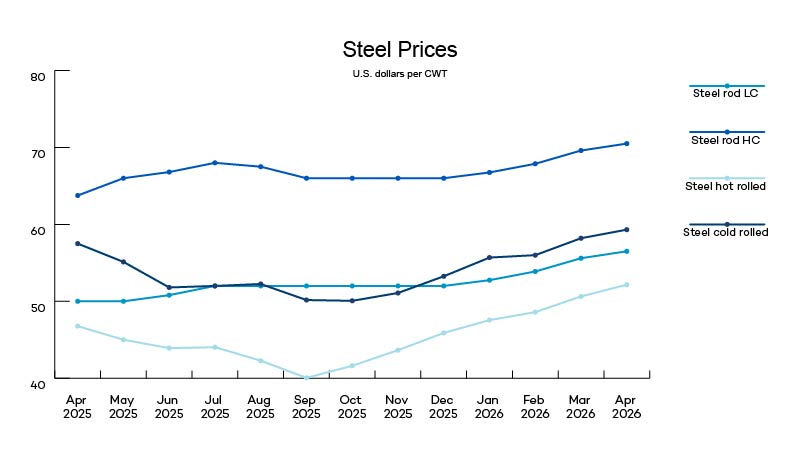

Trade tensions stall U.S.-Canada USMCA talks

The Canadian government announced a 1 billion Canadian dollar (nearly $734 million) loan program to support industries affected by U.S. tariffs on steel, aluminum and copper products.

Why it matters: The program aims to bolster Canada’s manufacturing sectors and safeguard economic sovereignty amid ongoing trade tensions with the United States.

Between the lines: Trade talks between the United States and Canada over renewing the United States-Mexico-Canada Agreement (USMCA) have reached a stalemate — compared to advances between the United States and Mexico — as both sides express “irritation” in each other’s trade policies, including U.S. tariffs of up to 50% on steel and aluminum products and forest products. Data from the Census Bureau reveals commerce between the United States and Canada accounts for approximately 13% of total U.S. trade.

By the numbers: The World Steel Association lowered its global crude steel demand forecast for 2026. The association projects global steel demand to grow by only 0.3% in 2026, down from the 1.3% forecast in October 2025, reaching 1.72 billion metric tons. For 2027, the association expects a 2.2% acceleration to 1.76 billion metric tons.

More steel news:

- The European Union approved a plan to cut tariff-free steel imports by nearly half to 18.3 million metric tons a year and to double tariffs on imports above that quota to 50% as soon as Wednesday, July 1.

- Trade officials and industry representatives from India contested claims of manufacturing overcapacity and production May 8 during a hearing at the Office of the United States Trade Representative (USTR). The hearing is part of a broader USTR investigation into trade practices and policies in manufacturing sectors from countries including India.

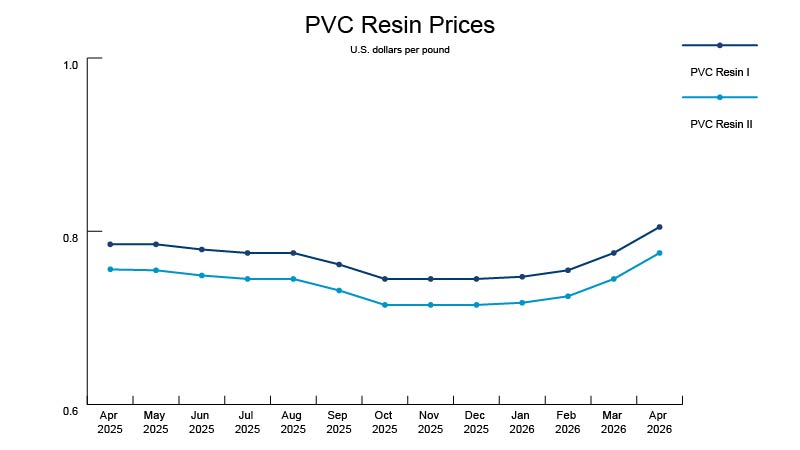

Resin prices expected to remain high throughout the year

High crude oil prices and the Strait of Hormuz blockade continue to impact the global resin market.

Why it matters: Despite a temporary ceasefire between the United States and Iran, structural supply issues persist, keeping prices elevated.

Zoom in: The global polymer market is experiencing unprecedented pricing changes driven by geopolitical disruptions rather than traditional supply-and-demand factors.

The big picture: Even if the conflict ends in the near term, resin prices are projected to remain high throughout the year due to ongoing supply disruptions.

News roundup

The Federal Reserve (Fed) voted 8 to 4 in April to maintain the benchmark funds rate between 3.5% to 3.75%, reflecting significant dissent among officials. Fed chair Jerome Powell said he will remain on the Fed Board of Governors until January 2028 after his term as chair ends later this month. Meanwhile, the Senate Committee on Banking, Housing and Urban Affairs advanced Kevin Warsh’s nomination to be Fed chair; a final confirmation vote will take place in the Senate, likely the week of May 11.